1926 – 2026 · Kelley Blue Book’s 100th Anniversary How the American auto market transformed — and why Kelley Blue Book was there for every turn.

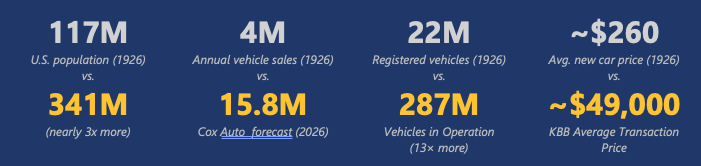

The 1920s were a transformative decade for the American automobile. Car ownership doubled. Closed-body sedans replaced open-air carriages. Technological innovations like electric starters and improved braking systems became commonplace — and for the first time, owning a car stopped being a luxury and was accessible to the middle-class.

What other lessons did that era teach us? And how do they echo today?

The Market: Then (1926) and Now (2026)

Data-Driven at the Core

Then: Making Cents with Sense

In 1926, The Blue Book was first published with appraisal values for vehicle acquisition. Data transparency was at the core of it then

Now: Same Question, Different Channels

The vehicles have changed. The sticker prices have certainly changed. But automobiles remain one of the most expensive purchases most people will ever make, and information remains the deciding factor in how confidently they make it.

Today’s buyers spend over 12 hours researching online before they visit a dealership. Over 80% of online car shoppers research prices before setting foot on a lot. Vehicle pricing data is more relevant than ever — giving transparency to dealers and buyers alike. A hundred years later, we’re still answering the same question: what is this car actually worth?

One in four new vehicle buyers used AI tools during their buying journey in 2025 — and that number is accelerating. As buyers turn to ChatGPT, Google Gemini, Perplexity, and others to answer questions like ‘what should I pay for this car,’ the answer they receive is only as credible as the data behind it. As we look ahead to the rest of 2026, visibility across all the major LLMs as a trusted, citable source of vehicle pricing and information is critical. Kelley Blue Book (KBB) is playing the same role it has played for 100 years, now in the channels where the next generation of buyers are starting their search.

Affordability

Then: The Price Drop That Changed Everything

In 1910, a Ford Model T cost more than $800, (roughly $27,000 in today’s money) too expensive for most working families at the time. Mass production changed that fast. By the mid-1920s, the same car cost $260, (about $4,800 today) still roughly 21–25 weeks of wages, but for the first time, within reach.

Now: Higher prices. More cross-shop

Today’s average new vehicle costs $49,191 (KBB, January 2026), and the Cox Automotive/Moody’s Analytics Vehicle Affordability Index puts the payoff time at 35.6 weeks of income — longer than a century ago. New-vs-used cross-shopping reached an all-time high at 43%, a signal that price pressure is driving buyers up and down and across the market.

Affordability shaped the car market in 1926, and it’s shaping it again now. When every dollar is being stretched, consumer advice, transparent pricing, and practical tools don’t just help consumers — they drive consideration. KBB’s role in that moment has never been more direct: intercepting buyers early, with independent data they can trust, before they’ve made up their minds.

The Car Becomes Personal — and Stays That Way

Then: More Than Just Better Horsepower (literally)

Before car ownership became widespread, American life was mostly localized-and those local areas were small. A horse-drawn trip. A streetcar line. The distance you could cover before you had to turn back. With widespread car ownership, it gave Americans the open road, and everything that comes with it: freedom and a sense of new possibility. Alfred Sloan’s vision at GM — “a car for every purse and purpose” — formalized this shift, aligning brands to different needs and lifestyles in a way that still shapes the industry today.

Now: A Dizzying Array of Choices

A car for every purpose has never been more true, or more complex. In 1926, the Model T alone represented roughly 40% of the market. Today, KBB tracks 48 brands and 481 distinct models-spanning subcompact to full-size, non-luxury to ultra-luxury, and every major powertrain from gas and hybrid to electric, plug-in hybrid, and fuel cell.

The range can feel overwhelming, and for most shoppers, it is. Only 37% begin their journey knowing exactly what they want. That uncertainty shows up clearly in how people shop. On KBB, Midsize SUV shoppers consider an average of seven other vehicles across three segments. Compact SUV shoppers evaluate nine vehicles across four segments.

In 2026, the challenge is helping shoppers navigate the many vehicle options available in the market. With 92% of buyers using content during their research, that’s exactly where KBB’s legacy of independent, data-informed advice matters most.

The trust Kelley Blue Book built over 100 years is the same trust buyers are looking for today — and it’s exactly what will carry our brand into the remainder of 2026, and the next century.

Thanks for coming on this ride with us. Here’s to another 100 years!

Sources: KBB Average Transaction Price Jan 2026 · Cox Automotive/Moody’s Analytics Vehicle Affordability Index Jan 2026 · Cox Automotive Car Buyer Journey Study 2025 · Cox Automotive Q1 2026 Industry Insights · FHWA Historical Data · Motor Magazine 1922 · BLS Historical Wage Series

Smarter content wins. Watch the Automotive News session to see how strategic content approaches are driving earlier influence, building trust faster, and keeping brands top of mind longer—insights that build on our one-sheet recap.

From tariffs to trade deals, the automotive market has seen no shortage of movement lately. What once felt like daily shifts in tariff and trade news has recently settled into a more week-to-week rhythm. We’ve seen both sales and shopper activity stabilize and are encouraged to see some positive year-over-year trends emerging.

With still a lot of lingering uncertainty, it’s no surprise that some marketers are wondering whether to tap the brakes and wait for things to settle. But here’s the good news: shoppers aren’t waiting. They’re still active, still engaged, and they’re showing us exactly what they need.

The Data Backs It Up

At Cox Automotive, we’ve been tracking consumer behavior across Autotrader and Kelley Blue Book, and the momentum is real. New vehicle shopping visits aren’t just holding steady; they’re outpacing last year’s levels. Even with economic uncertainty and tariff chatter in the background, shoppers are staying focused and engaged.

New Vehicle Sales Indicate an Active Market

Following the March 26th tariff announcement, we saw a clear spike in pull-ahead sales, a sign that buyers were ready to act fast to get ahead of potential price increases. That early burst of activity eased by late April but May brought a swift and promising rebound. It’s a powerful reminder that while headlines may cause momentary hesitation, they don’t erase demand. Shoppers are still in-market, and they’re proving that with the right conditions, they’ll keep moving forward.

Engagement Is Up, Even as Inventory Tightens

Even with early indications of a tighter supply, shoppers aren’t backing off. In fact, New Vehicle VDP pageviews are up year-over-year. Clear proof that interest isn’t just holding, it’s deepening. They’re not casually browsing; they are engaged and spending more time with listings, indicating a strong intent to purchase.

What’s Driving Demand is Need

Our latest Car Buyer Journey study shows that half of today’s shoppers are buying out of need, not want. And while the motivation is steady, what they’re buying is shifting. Affordability is now a top priority, with many shoppers leaning into non-luxury brands that offer practical value and long-term reliability. But that doesn’t mean the premium segment is fading – brands like Mercedes and Land Rover continue to hold their ground.

The top gainers? A healthy mix of domestic and import brands, premium and non-premium… signaling opportunity across the board.

The Road Ahead is Active And Full of Opportunity

Shopper behavior is sending a clear signal: they’re moving forward, even as the market shifts. They’re focused, pragmatic, and driven by real needs. Yes, external forces like tariffs, supply, and pricing will continue to evolve. But the fundamentals haven’t changed. People still need vehicles. They’re still researching, deciding, and buying. And they’re making it clear what matters most: affordability, availability and relevance.

This isn’t a moment for hesitation. It’s a moment to stay present, stay adaptable, and stay aligned with today’s shoppers. Because while the headlines may keep changing, the opportunity to connect, and convert, is right here, right now.

For over half a century, Earth Day has ignited a global movement, rallying millions to champion the planet’s well-being. The first Earth Day, celebrated on April 22, 1970, marked the beginning of environmental awareness. Today, 55 years later, Earth Day continues to inspire over a billion people worldwide to tackle the pressing environmental challenges of our time.

In automotive, there is no bigger task ahead than the shift to electrification. While there are still concerns about costs and charging infrastructure, sales show that more people are adopting EVs. In the first quarter of 2025, EV sales increased by 11.4% compared to last year. Interestingly, this growth is coming from brands other than Tesla. While Tesla’s sales declined, new models from Acura, Audi, Chevrolet, Honda and Porsche helped boost overall EV sales.

At Cox Automotive, we remain optimistic about the future. Despite some ups and downs, and starts and stops in regulations, we see a strong interest in EVs among consumers. Our data shows that an average of 4.4 million households have shown interest in electric vehicles over the past 90 days.

Autotrader has over 400,000 Electric and Hybrid vehicle listings from which consumers can shop, attracting hundreds of thousands of pageviews each month. Additionally, comScore reports that Cox Automotive has the highest reach among internet users who are interested in purchasing a new EV or Hybrid in the next six months, as well as the highest audience reach among people who indicated hybrid or electric-only vehicle capability as their top auto purchase factor.

Research and shopping for EVs on Autotrader and Kelley Blue Book have remained stable, with a 9% increase in New Car Visits year-over-year. Similarly, we’ve seen Hybrid and Plug-In Hybrid shopping increase by 11% year-over-year. While interest varies across different regions in the U.S., we’ve seen an increase in EV and Hybrid shopping across all Census Regions, even with lower gas prices.

The road to electrification certainly has not been a linear progression, but there’s a lot to be optimistic about with exciting new products and a robust and growing consumer base. On Earth Day, we’re reminded that the path to a more sustainable future isn’t just paved with good intentions – it’s driven by informed action. As EV adoption accelerates, we all have a powerful role to play in shaping a greener tomorrow.

Download our latest EV and Hybrid shopper data and explore advertising opportunities with Cox Automotive to reach this highly engaged audience. Together, let’s drive the change and shape what’s next.

The Car Buyer Journey is one of our longest running studies, marking its 15-year anniversary this year. Over this extensive period, the study has continuously evolved, yet our core objective remains unchanged: to understand how consumers purchase vehicles and to share these valuable insights with our clients and the industry.

The Journey Continues

In this study, we examine the car buying journeys of over 1,500 new vehicle buyers, including nearly 700 non-luxury import buyers, 400 non-luxury domestic buyers, and 450 luxury buyers. Our research has uncovered five key takeaways that are currently shaping consumer buying behaviors.

Key Takeaways

Buyers shop options as inventory & incentives rise: With new vehicle inventory more than doubling compared to two years ago, limited inventory is no longer a significant obstacle for most buyers, with only 30% of buyers mentioning it as a concern. Buyers are keeping their options open, with cross-shopping between new and used vehicles at 37%, driven by an increasing number of attractive deals.

Buyers dedicate more time to the shopping journey: In 2024, new buyers spent an average of 2 hours more on the shopping process compared to the previous year. This significant increase is driven by buyers investing more time in test driving and exploring new product features, rather than focusing solely on price negotiation. This shift indicates a growing interest in understanding and experiencing the vehicles before making a purchase decision.

Third party sites widen their lead as top source: As new vehicle inventory and prices have fluctuated, buyers are dedicating more time to research. Third-party sites have surged ahead, becoming the top online source at 72%.

Omnichannel experience is more seamless: While few new shoppers initially plan to complete their purchase entirely in-person, 51% of buyers end up doing so. The main reasons for this shift from online to in-person purchasing are:

Test Drives – Once buyers come in for the test drive, they often find it more convenient to complete the transaction at the dealership.

Direct answers – New buyers prefer working directly with the dealers to get answers to their questions, as they feel not all pertinent information is available online.

Buyer satisfaction reaches an all-time high: The percentage of buyers who were highly satisfied with their shopping experience has reached 75%, marking an all-time high in the past 9 years. Changes made to the online shopping process during the pandemic have had a significant impact on this increase.

Growth in aftermarket products & service loyalty: With increased buyer satisfaction, we’re also seeing continued growth with aftermarket products, extended warranties, and service contracts, especially among non-luxury domestic buyers. Our data shows that 82% of buyers are likely to have their vehicle serviced at the dealership of purchase. Additionally, buyers who have visited the dealership’s service department within the 12 months prior to deciding to buy are more inclined to purchase from the same dealer again.

Embrace the Digital Shift

The advantages of completing more of the car buying process online are undeniable. It saves time, enhances transparency and ensures a smoother transition from online shopping to in-store purchasing. New buyers report they are increasingly more satisfied with this seamless experience.

In fact, 78% of new buyers rated their experience of picking up in-store where they left off online as highly satisfactory. It’s important to encourage your dealers to digitize and automate their processes and to provide them with access to effective partners who can facilitate this transformation.

Where to Next?

As the needs and preferences of car buyers evolve, it’s important to meet them where they are. Make the buying process so seamless that it’s harder for them not to buy from you. Ready-to-buy consumers are not just on dealer sites, so its essential to provide multiple entry points into the purchase funnel. Begin with third-party listing sites for their extensive reach, but also focus on integrating direct retail capabilities into your own website.

Stay Ahead of the Curve

To stay ahead in the automotive industry, it’s important to understand the customers’ preferences, to help guide them along their journey. Buyer satisfaction is at an all-time high, and a Cox Automotive Marketing Partnership provides you with the tools and insights to keep you ahead of that curve. Our consumer data and dynamic content allow you to create personalized marketing strategies that build trust and loyalty with shoppers, helping them make smart decisions that align with their evolving needs.

By leveraging the insights from the Car Buyer Journey study and partnering with Cox Automotive, you can navigate the twists and turns of the market, ensuring your strategies remain impactful.

For more insights and marketing tips, download our Car Buyer’s Journey infographic, or click Learn More to download the full study.

Did you know that the Big Game pulled in an audience averaging 126 million viewers this year? With Fox commanding a record ad price of $8 million (and in some cases more) for a 30-second spot, it’s no wonder that the stakes are higher than ever. However, as evident by a shrinking number of participating OEMs, this price point is steep. In a time where automakers are looking for more efficiency, advertising in the Big Game might feel like a Hail Mary. But is it worth the gamble?

When automakers advertise in the Big Game, it’s not like convincing a consumer to buy a bag of chips or make an impulse buy. In automotive, we are talking about much higher price points and detailed lifestyle considerations. It cannot be a one-and-done event. Advertisers need to follow up that awareness play to help generate more shoppers for their respective brands.

Momentum is hard to sustain. Often, we see a burst on GameDay, but sometimes we don’t see meaningful shopping activity impact in the days and weeks that follow. We’ve seen lifts over 10,000% for debut car models, and exponential lift for established car models. The momentary lift can be staggering but short-lived. We’ve seen the most success with model specific ads – compared to brand spots or ads featuring halo vehicles, which are sometimes too expensive for most consumers.

While the goal and intent of any Big Game ad varies, when the goal is to sell more cars, or sustain brand momentum – Big Game ads should be reinforced where consumers are shopping. Cox Automotive sees 28M+ unique visitors each month across Autotrader and Kelley Blue Book. Automakers who reinforce their Big Game ads on sites like Autotrader and Kelley Blue Book see sustained lift* for the month of and following the Big Game.

Here’s an example of some of the lift metrics we’ve seen

+40% organic lift to Kelly Blue Book VDPs from a client campaign

+400% Increase in Research Activity for the Advertised Model on Kelly Blue Book

+36% Increase in Shopping Activity for the Advertised Model on Autotrader

+397% Lift in total visits for Dealer.com

So, while the initial impact of a Big Game ad may be impressive, the key to long-term success lies in the follow-up. By strategically reinforcing those ads on platforms where consumers are actively shopping, automakers can turn that momentary lift into sustained momentum. The Big Game may be the kickoff, but the real game is in the follow-up.

They say the Big Game is the biggest night in sports—unless you’re a Denver Broncos fan like me, in which case it’s more of a nostalgic event where we reminisce about the glory days of John Elway and try to forget about, well… Big Game XLVIII against the Seahawks. (Hey, at least we made history for the fastest score ever—just, you know, not the way we wanted.)

But while some teams struggle to make the most of their Big Game moments, automotive advertisers don’t have to. Thanks to Connected TV (CTV) advertising, Cox Automotive is unlocking a game-changing opportunity: delivering dynamic ad messages tailored to different shoppers based on where they are in their car-buying journey.

The Evolution of Advertising: Reaching the Right Shopper at the Right Time

In the past, advertising was a one-size-fits-all approach. A single TV commercial would air to millions of viewers, hoping that a fraction of them were in-market for a car. But today’s digital ecosystem gives us the ability to serve hyper-targeted CTV ads to households that have already identified themselves as car shoppers.

Instead of guessing, we can now serve distinct ad experiences based on where shoppers are in their journey allowing for the message to resonate. Let’s look at how we are doing it with three distinct Cox Automotive signals:

Low-Funnel Shoppers (Ready to Buy)

These are consumers who have actively engaged with Cox Automotive websites, viewed inventory, or checked financing options.

Ad Message: “Final offers,” real-time dealership inventory, trade-in promotions, and calls to action like “Schedule a Test Drive.”

Mid-Funnel Shoppers (Actively Shopping)

These are shoppers who are researching models, comparing features, and engaging with online vehicle reviews.

Ad Message: Lease and finance options, vehicle comparisons, and dealership incentives to guide them toward a decision.

High-Funnel Shoppers (Just Starting Their Journey)

These consumers are casually browsing, considering different makes and models, and engaging with automotive content.

Ad Message: Brand-building, lifestyle-focused creative, and emotional storytelling to create future brand preference.

CTV: The Smartest Way to Advertise in Today’s Digital Landscape

This isn’t just about targeting—it’s about delivering the right message to the right audience at the right time. Having three distinct ad strategies within an individual market ensures that every household gets a relevant ad experience that matches their current buying process. So, instead of spending millions on broad-reach advertising that hopes to resonate with a fraction of the audience, this CTV solution enables automotive advertisers to maximize their return on ad spend by speaking directly to engaged, in-market shoppers with messages tailored to their intent.

A Smarter Approach to Big Game Advertising

Gone are the days when advertisers had to throw a message out to a massive audience and hope it sticks. With CTV, automotive brands can ensure that every Big Game ad dollar is working harder, reaching the right households with the right messaging. Like a great football team adjusts its strategy based on the game situation, advertisers today have the tools to be more strategic than ever before. By leveraging CTV’s ability to deliver custom messaging based on actual shopper behaviors, automotive brands can drive stronger engagement, better conversion rates, and more efficient ad spending.

This isn’t the future of advertising—it’s already here. For OEM or dealers looking to maximize impact during high-profile events like the Big Game, CTV is the smartest play in the modern digital landscape.

Want to learn how Cox Automotive can help you tailor your CTV strategy for maximum impact? Let’s connect.

Did you know that over 80% of consumers believe that macrotrends will reshape car buying in the next decade? As our needs and behaviors evolve at an unprecedented pace, it’s crucial for industry leaders to stay ahead of the curve. Whether you’re an OEM, dealer, or lender, understanding these shifts is key to meeting the demands of tomorrow’s consumers.

Cox Automotive surveyed over 2,000 consumers about their current car shopping attitudes and how they expect these to change over the next 10 years. Our research focuses on major changes with widespread impacts.

Customers’ Needs are Driven by Defining Moments

The needs of consumers today are very different from those of just 4 years ago, and the consumers of tomorrow will have new expectations and preferences. This evolution is shaped by the significant events we’ve experienced and those we will encounter in the future. The most impactful changes are those that span multiple industries and will sustain over time. These are what we call macrotrends.

Macrotrends Have Widespread Impacts

These trends were selected because they are reshaping every aspect of our lives, including car buying. We asked these consumers how they pictured their lives in 10 years, relative to these macrotrends.

Trust & Transparency: Personal data is fueling all our experiences. People feel more exposed and expect companies they trust to prioritize their privacy and protection over profit. A significant 77% will only share data with companies that are transparent with their privacy policies.

Shifting Needs: Consumersare rethinking how products are used and how they shop for them, prioritizing flexibility and convenience. For example, 61% would be comfortable buying entirely online, especially younger buyers.

Redefining Affordability: With money not stretching as far as it used to, consumers are more selective in their spending. For many, affordability is no longer about “what can I afford?” but rather “what do I want to afford?” In fact, 62% are willing to indulge in their next vehicle, if it makes them feel good and improves their quality of life.

Environmental & Social Causes: More people today are holding businesses accountable to act toward a greener, more inclusive and equitable world. About 65% pay attention to the environmental impact of their purchases.

Immersive Experiences: Technological innovation, such as Augmented Reality (AR), Virtual Reality (VR), and Artificial Intelligence (AI), is driving change. Around 55% are comfortable using chatbots for routine questions within the vehicle shopping experience.

Impact of Macrotrends on the Future of Car Buying

Consumer behavior in vehicle shopping has changed significantly and will continue to evolve over the next decade. As younger generations become a larger percentage of car buyers, OEMs must be prepared for these shifts. While consumers predict a rise in “all online” purchases, omnichannel experiences are expected to remain the most popular.

Ultimately, OEMs and dealers will need to support all online purchases, as 1 in 3 buyers prefer this path. However, with a 43% preference, omnichannel remains the favored method, even when looking 10 years ahead.

Embracing the Future

To stay ahead in the automotive industry, it’s important to understand and adapt to these big trends. A Cox Automotive Marketing Partnership gives you powerful tools and insights to keep you ahead of the curve. Our consumer data and dynamic content allow you to create personalized marketing strategies that build trust and loyalty with shoppers, helping them make smart decisions that align with their evolving needs.

The future of car buying is already here. Together, we can shape it by connecting every moment, understanding every need, and making the car buying experience smooth and enjoyable for everyone.

Electric vehicles are becoming more mainstream, but growth is hitting a speedbump.

It’s been an exciting time in the industry as electric vehicle (EV) sales hit new records. For the first time, in 2023, over a million EVs were sold. Fast forward to January 2024, and now there are more than 3.2 million EVs in the U.S. 1 More EV models are entering the market from more manufacturers, which means pricing is getting more competitive and more people can afford them.

Yet the EV growth rate is slowing. An increase in supply and more available models have outpaced consumer demand. With weakening demand, Tesla led the pack in making price cuts and began a domino effect across the industry. EV consideration among car shoppers has begun to wane and inventory is sitting on dealership lots longer. So what’s next for the EV market?

Many consumers aren’t ready for EVs…yet.

An EV Skeptic is defined as a car shopper who is only considering vehicles powered by traditional internal combustion engines (ICE). According to the 2024 Path to EV Adoption Study by Cox Automotive, nearly half of vehicle shoppers in the market today are Skeptics. These shoppers are apprehensive about the idea of fully committing to an electric vehicle.

Why aren’t most car buyers ready to take the leap into the electric vehicle segment? There are multiple barriers to adoption that OEMs and dealers will need to overcome to move Skeptics into a consideration and purchase mindset:

Driving Range and Lack of Infrastructure – Consumers are still worried about the range for electric vehicles and that they won’t be able to drive as far. Notably, there is still widespread concern that a lack of charging stations could impact their travel plans.

Battery Fears – EV batteries continue to serve as a deterrent to purchase due to concerns about the battery losing charge, the length of time to charge as well as the cost to replace the battery.

Affordability – While purchase price is coming down and the addition of more models provides more affordable options, consumers still perceive ownership costs for EVs to be higher than comparable ICEs and hybrids.

These perceptions continue to make consumers apprehensive about EVs so many are still looking to the familiarity of ICE and hybrids for their next vehicle.

But there is still hope for an EV future. How can OEMs encourage car shoppers to take the leap?

While growth has slowed, for many brands, awareness and consideration of EV models is strengthening. This could signal that more consumers will look toward EVs sooner than later. EV consideration will notably increase with 54% of current Skeptics saying that 3-5 years from now will be the right time to purchase an EV. By 2033, 90% of vehicle shoppers will be considering an electric vehicle.2

This shift will be driven by continued advances in technology, more EV charging infrastructure and consumer education. More models and price reductions will cast a wider net attracting Gen Z, multicultural and less-affluent shoppers.

Educating consumers on EV ownership will be key in driving this shift. OEMs and advertisers can start now to nudge them into the consideration stage.

Content helps EV buyers make decisions.

EV buyers consume more content than ICE buyers. They rely heavily on content, especially videos, when researching online. Expert reviews and ratings, vehicle awards and more help consumers better understand the new world of electric vehicles. New EV buyers also visit more sites than new ICE buyers as they gather information.3

Powerful video advertising and content leads EV buyers to take actions like contacting or visiting a dealer, looking up more information on a vehicle, submitting a form and scheduling a test drive. 74% of new EV buyers took action after viewing an online auto video ad compared to 65% of new ICE buyers.4

Your EV content should highlight your brand’s line up. With more models entering the market, consumers need to know what sets yours apart. EV considerers tend to be technology focused. Spotlighting tech enhancements and features in your line up is a critical way to move shoppers closer to purchase.

Call out the key benefits of electric (EV) versus internal combustion (ICE) vehicles. As EV shopper demographics are skewing younger, lower income and multicultural, helping these audiences understand the benefits of EV will move them closer to their purchase.

Entice EV shoppers and skeptics with key offers.

Free charging and maintenance offers could help push both EV Considerers and Skeptics closer to purchase. A free at-home charger, free maintenance or service plan, as well as free charging at charging stations are concepts that would help increase EV sales with consumers. Survey respondents indicated that six months of free maintenance and free charging would be the optimal trial period.2

Accelerate EV adoption with coordinated efforts across OEM and Dealer levels.

67% of franchise dealers prefer that OEMs share in the responsibilities for upper funnel activities, while they take charge of the lower funnel steps.2 Dealers want OEMs to help educate consumers on their line-up, on the key differences and benefits of EV vs. ICE, as well as provide information on EVs listed for sale.

Get Ready for the Switch

While maybe not as quickly as OEMs and dealers would like, the automotive shopper is moving toward the new frontier of electric vehicles. Understanding and addressing why Skeptics and Considerers are delaying an EV purchase can help you entice them to purchase sooner. Brand and model content tools, especially video, will be critical to educate, build awareness and drive higher consideration. Higher incentives and working across tiers will move shoppers closer to an electric future.

With elevated vehicle prices, CPO vehicles have become more attractive to buyers who don’t want to spend new car money but want the peace of mind that comes with warranty protection.

It’s becoming harder than ever to afford a new vehicle. The average American who bought a new car in September signed up for a $738 monthly payment. That’s a record high for consumers to consider when determining if they can afford one.

But that doesn’t mean that life stops just because there’s higher monthly payments, tight inventory, and fewer incentives. Despite these headwinds, consumers still need vehicles, and they’re willing to change their minds for the right opportunity.

As your trusted partner, Cox Automotive is right there alongside you to help navigate changes in the automotive industry, so that you can still drive more engagement with the consumer and continue to deliver more vehicle sales. With that in mind, let’s take a deeper look at what’s shaping up to be big CPO opportunities for 2023!

“ Demand remains robust for certified vehicles as the new market continues to be very supply constrained and CPOs offer the best substitute for consumers.”

– Jonathan Smoke | VP Chief Economist | Cox Automotive

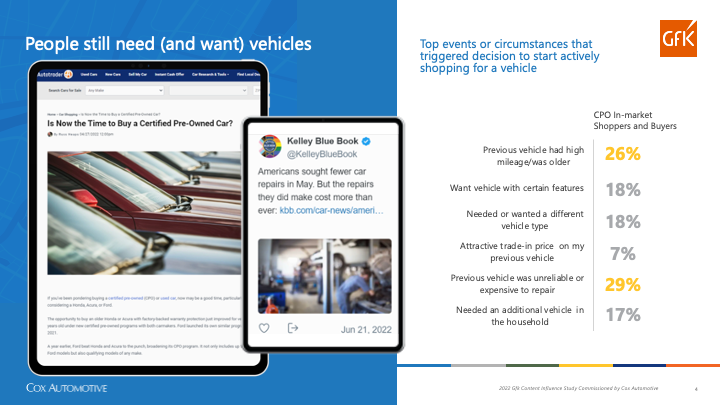

Shoppers Still Need Vehicles

First the good news…shoppers still need vehicles, and there are many reasons that triggered Certified Pre-Owned shoppers to enter the market.

Our 2022 Gfk Content Influence research shows that the top reasons these CPO shoppers entered the market were:

29% – their previous vehicle was deemed unreliable or deemed too expensive to repair?

26% – triggered due to their previous vehicle having high mileage and/or it was older?

These shoppers can’t afford to wait for a better price. They know prices are high, and unfortunately, they can’t delay for that long.

CPO vehicle interest increases, and cross-consideration intensifies

The new car market continues to feelthe impacts of high-inflation and elevated prices, which is also making CPO vehicles more attractive to buyers who don’t want to spend new car money, however, want the peace of mind that comes with warranty protection. And we’re seeing a rising interest for certified vehicles on Autotrader:

Most impressive were the September CPO results:

+17% VDP Visitors Year over Year?

+26% Vehicle Details Page Views Year over Year?

Pencils are up +76% Year over Year?

Something else that should be on our industry’s radar, as interest increases, many shoppers are considering multiple brands and segments to find a vehicle that meets their needs. So getting in front of the CPO buyer, as well as staying side by side with them throughout their car purchase journey, should be a priority.

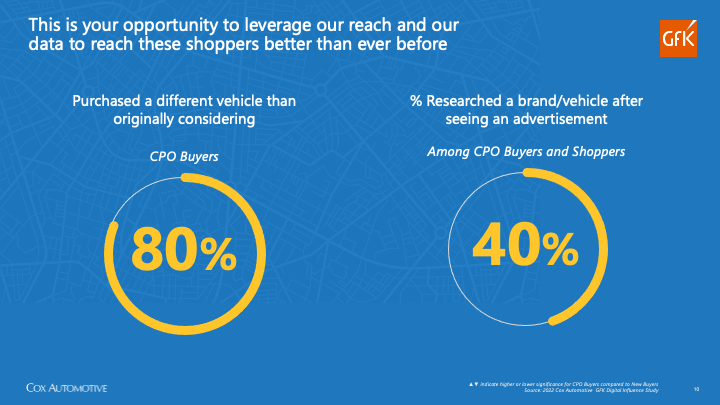

CPO Car Shoppers are Willing to Change Their Mind

A key thing all OEM’s and Dealers need to be aware of is that even in today’s market conditions, our 2022 Digital Influence research with GFK shows that car shoppers are still willing to change their minds for the right opportunity. You not only need to know if your vehicle is in their consideration set, but also what you’re up against competitively, from brand preference to inventory availability.

It’s a staggering statistic that 80% of CPO buyers bought vehicles that were different than what they originally considered. And just as important to call out, automotive advertising has persuaded them to research vehicles after exposure. Especially on third-party sites, which are valuable in helping shape brand decisions.

40% of CPO customers stated auto ads motivated them

to research a different car than they originally considered

That’s right… 2 out of every 5 CPO customers stated automotive ads motivated them to research a different car than they originally considered. This data should give you an extra incentive as you plan the year ahead to not only stay in front of your target audiences, but put an increased focus on getting in front of new audiences. Because the brand they thought they wanted to purchase, might not end up being the brand they ultimately purchase.

Where the Majority of a CPO Purchasers’ Time is Spent

Although the decision and purchasing timeframes have shortened over time, we now see more time devoted in the exploration phases for a CPO purchaser. Working with a partner to find shoppers further out from purchase, before they’re even giving you an indication that they’re doing anything, will offer the greatest opportunity for influence.

CPO buyers reported they spent the most time trying to find actual vehicles for sale, which should be of no surprise due to tight inventory. Of equal interest is that they are also heavily comparing different models by researching reviews, options, and pictures, as well as researching vehicle pricing.

Here are the Top 4 Activities research shows a CPO buyer spent the most time doing:

Find actual vehicles listed for sale

Compare different models using reviews, options or pictures

Research vehicle pricing

Browse vehicle images

CAMP 360 – Data That Drives

Cox Automotive understands your CPO shoppers. And with your partnership, our data can make your data drive efficient and more informed marketing decisions.

Your marketing partnership follows CPO buyers along the full purchase horizon, every step of the way. We’re seeing half of CPO site visitors 6+ months out from purchase, which is the optimal time to reach and influence them, before they have decided. It’s why you need a first-in-class data partner to help you find those shoppers, to not only get their attention, but keep their attention.

It’s more important than ever for advertisers to be front and center at the critical decision points along the CPO’s car purchasing journey in order to influence consideration and reinforce brand loyalty. Especially as you focus on your marketing strategy for 2023.

Because with the power of your Cox Automotive Marketing Partnership alongside you, our successes, data, audiences and destinations can be yours. Powered by advanced AI learning capabilities and proven by transparent reporting, CAMP 360 utilizes first-party data across the entire customer journey to ensure the right CPO message and content is reaching, and most importantly, resonating with CPO shoppers in the moments that matter most.

Sources:

2022 Gfk Content Influence Study Commissioned by Cox Automotive

2022 Gfk Digital Influence Study Commissioned by Cox Automotive

Autotrader September 2022 Site Metrics

COX Auto BTR based on Drive IQ; Visits = January 2021 – Dec 2021; Sales = January 2021 – Aug 2022

Are you ready for data that drives? To seamlessly integrate content and native advertising within a personalized environment? If so – find out more about a CAMP 360 data-driven marketing partnership by clicking HERE.